MENU

MTD for Income Tax

SERVICES

Audit and Assurance

Business Support

Business Tax

Corporate Finance

Corporate Tax Advisory

General Practice

Payroll

Private Client Tax

Probate and Estate Administration

Start Ups

Tax Fee Protection Service

Wealth Management

IT Solutions

SECTORS

Agriculture

Construction

Contractors

Creative Industries

Manufacturing

Not For Profit

Property

Retail

Road Haulage

Technology

UK Subsidiaries

ABOUT US

Our Purpose and Approach

Practice History

Office Locations

Our Partners & Associates

Client Google Reviews & Testimonials

Fees

Vacancies

CONTACT US

Client Payroll Portal

Sign Up

MTD for Income Tax

SERVICES

Audit and Assurance

Business Support

Business Tax

Corporate Finance

Corporate Tax Advisory

General Practice

Payroll

Private Client Tax

Probate and Estate Administration

Start Ups

Tax Fee Protection Service

Wealth Management

IT Solutions

SECTORS

Agriculture

Construction

Contractors

Creative Industries

Manufacturing

Not For Profit

Property

Retail

Road Haulage

Technology

UK Subsidiaries

ABOUT US

Our Purpose and Approach

Practice History

Office Locations

Our Partners & Associates

Client Google Reviews & Testimonials

Fees

Vacancies

CONTACT US

Client Payroll Portal

GO

Latest Audit and Assurance

Our Content

Close Company Dividend Reporting Changes

From the 2025/26 tax year, HMRC has introduced significant changes to how dividends from close companies are reported on...

James Selby

Bury’s 2026 Sports Evening & BBQ

On Tuesday 7th July, colleagues from our Bury St Edmunds office came together for a sports evening and BBQ at the British Sugar...

Matthew Oakley

Change to Probate Fees

The Ministry of Justice has announced an increase to Probate Fees. This came into effect on 13 July. To apply for a...

Sheryl Lewis

Winter Fuel Payment Charge

Overview From 6 April 2025, pensioners with total income exceeding £35,000, and who are not in receipt of a qualifying benefit,...

Beth Fischer

Geopolitical Events and Global Stock Markets

How Geopolitical Events Influence Global Stock Markets - And Why Staying Invested Often Wins Global markets dislike surprises....

David Salmon

Foreign Income and Gains (FIG) Regime: From 6...

What is the Foreign Income and Gains (FIG) regime? The 2024 Spring Budget stated there would be changes to the domicile-based...

Beth Fischer

Government Funding for Peatlands Announced

The Government has announced £47 million of funding to be used to protect and improve peatlands in England. As peatlands...

Paul Wood

Proposed Key Tax Changes

The government has unveiled a package of proposed tax and customs reforms designed to reduce administrative burdens, improve...

James Selby

Time to Take Action: Making Tax Digital (MTD) for...

The first quarter for Making Tax Digital has ended and it is time to make that first submission. The first quarter ending 30th...

Maddie Milner

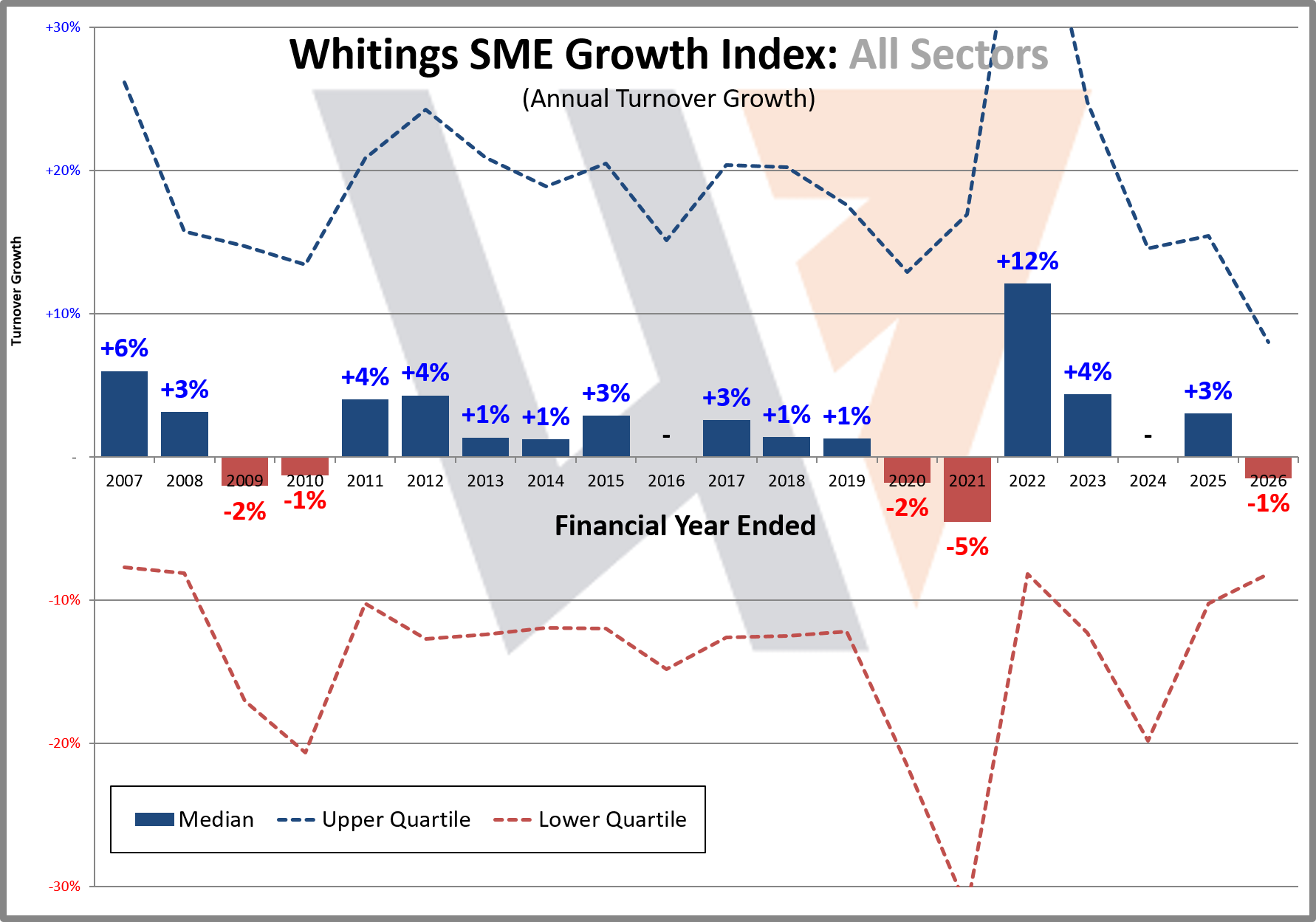

2026 SME Growth: New Head Winds ?

(data source) As we pass the half way point in 2026 we now have enough data to re-assess the financial health of our SME business...

Ian Piper

1

2

3

4

Next »

Request a Call Back from