New Audit Exemption Thresholds: What Could This Mean For You?

15th July 2024

15th July 2024

Have you heard about the new audit exemption thresholds?

Before the recent General Election the Conservatives announced plans to increase the audit exemption thresholds. For the Turnover and Gross Assets thresholds, this increase is significant (50%), effective for accounting periods starting on or after 1 October 2024. For certain growing companies, this presents an opportunity to extend their current accounting reference date, to take advantage of these thresholds earlier than would occur naturally.

However, this change, which was planned to be enacted (within The Companies (Non-financial Reporting) (Amendment) Regulations 2024) during the Summer, did not happen before the Election. And as we now have a different Government and not much Parliamentary time left before the Summer recess, progress is now uncertain. So, it may be worth delaying this decision until at least 1 August 2024.

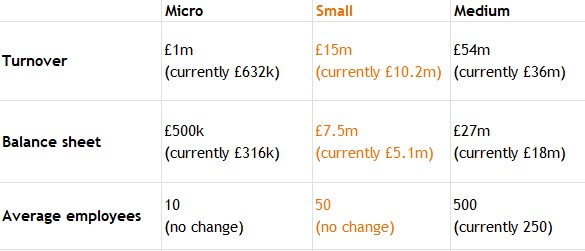

From 1 October 2024, the new size limits are to be as follows:

You cannot extend a period so that it lasts more than 18 months from the start date of the accounting period (unless the company is in administration).

You may not extend more than once in 5 years unless:

- the company is in administration

- the Secretary of State has approved this

- the company is aligning its accounting reference date with that of a subsidiary or parent undertaking under the law of the UK

Get In Touch

Contact your local Whitings office today for information and advice on how the changes to audit exemption limits could affect you.